2026 California State Disability Insurance (SDI) Tax Guide

The State Disability Insurance (SDI) withholding rate has increased to 1.3% for 2026, with no wage cap. Learn how California SDI taxes apply to your paycheck this year.

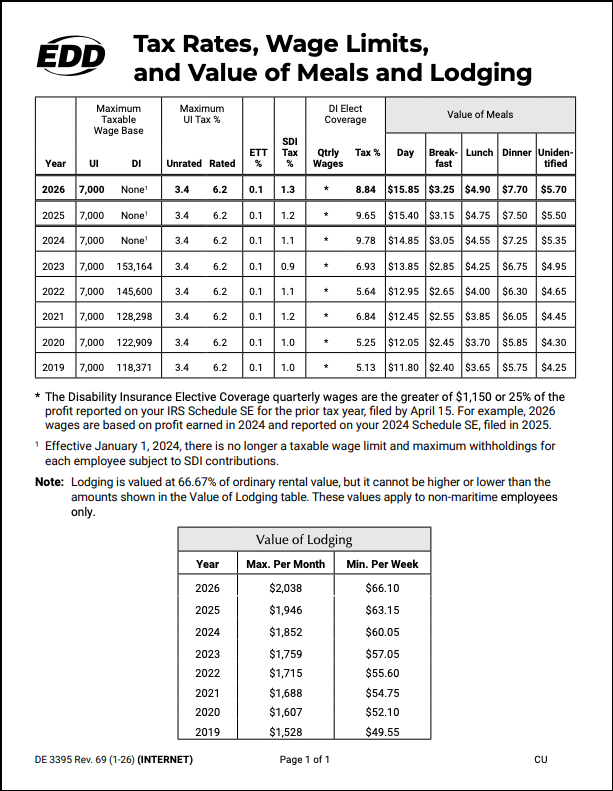

In 2026, all wages earned in California are subject to State Disability Insurance (SDI) contributions—with no maximum wage cap for the third straight year. This year’s SDI tax rate is 1.3%, meaning California workers now contribute a slightly higher percentage to support disability and Paid Family Leave benefits compared to last year.

In this guide, we explain how SDI tax is calculated, who pays it, and how it fits into California’s broader system of payroll taxes. For benefit details—including new payout levels and the increased maximum weekly benefit in 2026—see our 2026 SDI benefits guide.

What is SDI and how is it taxed?

California’s State Disability Insurance (SDI) program provides partial wage replacement to workers who can’t work due to:

- Non-work-related illness or injury

- Pregnancy and childbirth

- Bonding with a new child or caring for an ill family member (Paid Family Leave)

Unlike some other payroll taxes, SDI is funded entirely through employee wage deductions. Employers are responsible for withholding the correct amount, remitting it to the Employment Development Department (EDD), and ensuring compliance.

2026 SDI tax rate and wage base

For 2026:

- SDI withholding rate: 1.3% of gross wages

- Wage limit: None (all wages are subject to SDI)

- Maximum annual contribution per employee: Unlimited (depends on total wages)

This follows the significant structural change that began in 2024, when Senate Bill 951 removed the taxable wage ceiling for SDI contributions to expand benefits for low- and middle-income Californians.

How SDI fits into California payroll taxes

SDI is one of four state payroll taxes that employers and employees must manage. While SDI is an employee-funded program, it is part of a broader system of withholdings and contributions:

| Tax Type | Who Pays | Purpose | 2026 Rate/Limit |

|---|---|---|---|

| Unemployment Insurance (UI) | Employer | Temporary support for laid-off workers | 1.5% – 6.2% on first $7,000 |

| Employment Training Tax (ETT) | Employer | Funds employee training and skill development | 0.1% on first $7,000 |

| State Disability Insurance (SDI) | Employee | Wage replacement during non-work disability or family leave | 1.3% / No Cap |

| Personal Income Tax (PIT) | Employee | Funds state services like schools, parks, and healthcare | Based on Method A/B |

Chart: SDI and Payroll Tax Rates Over Time

The official EDD chart shows that the SDI tax rate has increased slowly, but consistently, in the last three years, from 1.1% in 2022 to 1.3% in 2026. Notably, last year's removal of the SDI wage ceiling means high earners will contribute significantly more toward the program.

Why is the SDI cost increasing?

The 2026 increase to 1.3% continues the implementation of Senate Bill 951, which was designed to make the program more equitable for middle-income Californians. By removing the taxable wage ceiling and slightly adjusting the rate, the state has been able to increase the maximum weekly benefit and ensure that low-to-middle-income workers receive a higher percentage of their wages while on leave.

Employer obligations for SDI

For 2026, California employers must adhere to the following requirements:

- Withhold 1.3% of gross wages from all employees regardless of total income.

- Remit SDI withholdings to the Employment Development Department (EDD) according to their designated filing schedule.

- Maintain accurate records of all wages paid and taxes withheld.

- Provide new hires and existing employees with updated information regarding SDI and Paid Family Leave eligibility.

SDI vs. Paid Family Leave: What’s the difference?

Paid Family Leave (PFL) is technically a component of the SDI program. While SDI traditionally covers your own disability or illness, PFL covers you when you need to care for others. In 2026, you may qualify for PFL if you are:

- Caring for a seriously ill family member (child, parent, spouse, etc.).

- Bonding with a new child (birth, adoption, or foster care).

- Participating in a qualifying event resulting from a family member’s military deployment.

Your employer withholds the same 1.3% for both programs; your eligibility is determined by the specific reason you file your claim.

Summary of 2026 Key Figures

The following table outlines the estimated benefit tiers for 2026 based on the new maximum weekly benefit of $1,765.

| Annual Income | Highest Quarterly Wages | Weekly Benefit Amount |

|---|---|---|

| Less than $1,200 | Less than $300 | Not eligible |

| $1,200 – $2,889.96 | $300 – $722.49 | $50 (Minimum) |

| $2,890 – $65,119.60 | $722.50 – $16,279.90 | 90% of weekly wages |

| Over $65,119.60 | Over $16,279.91 | 70% of weekly wages, max of $1,765/week |